DCASH: Towards A Digitally Inclusive Future

By Karina A Johnson

Key Messages

- CBDCs can bring efficiency, speed and connectivity to our use of money both within and beyond the ECCU

- DCash was introduced as a component of the ECCB’s payments system modernisation

- Digital finance ecosystem development increases the utility of a retail CBDC in the ECCU

- The DCash pilot showed that digital financial inclusion is the way to go

We Cannot Stand Still

The Eastern Caribbean Currency Union (ECCU) has long been a model of monetary stability, thanks to the strength of the Eastern Caribbean dollar, which has been pegged to the United States dollar (US$) since 1976 at a rate of US$1.00 to EC$2.70. However, at the Eastern Caribbean Central Bank (ECCB), we know that stability is not about standing still, but about evolving to better meet the needs of the people we serve.

Over the past two decades, the financial landscape has transformed dramatically. Fewer banking branches mean less access for customers, while a growing number of unbanked individuals and micro, small and medium enterprises (MSMEs) are left underserved. Add to that the rise of the gig economy[1], the urgent need for stronger regional trade in goods and services, and global shifts like digital technology advancements, big tech’s foray into finance, and the explosive growth of cryptocurrencies and decentralised finance (DeFi). It becomes clear: we must innovate or risk becoming casualties of displacement.

In 2018, ECCB set out on an ambitious mission: to modernise our retail payment system. A key component of this mission was the creation of a solution as reliable as the EC dollar but faster, easier to use and more accessible than current payment methods—even to those without a bank account. At the time, central bank digital currencies (CBDCs) were barely on the radar of most central banks, but the ECCB embraced an opportunity to lead.

A Leap Forward

By early 2021, working with a technology service provider, the ECCB had developed and was testing internally a digital currency and retail payment system to create a digital EC dollar. It was named "DCash," an amalgamation of "digital" and "cash." DCash utilised blockchain technology, which is a type of distributed ledger technology that ensures security and prevents issues like double spending—essential features for a CBDC. Like cash, DCash was designed to satisfy the core functions of money:

- transfer of value between parties

- store of value

- unit of accounting that facilitates comparison of the value of different goods and services

Unlike cryptocurrencies, whose volatility erodes their usage as a store of value, DCash would continuously maintain 1:1 parity with EC notes and coins.

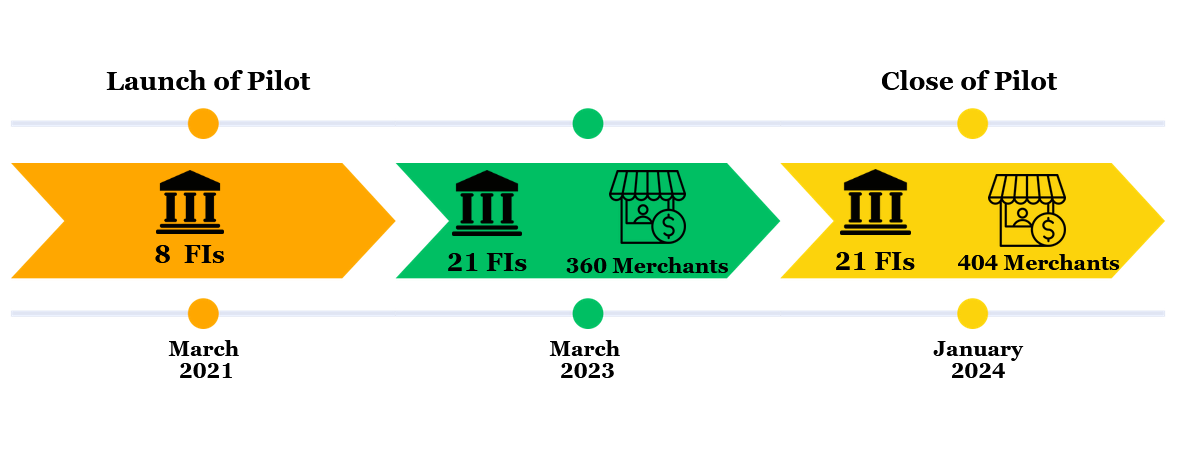

Then came the COVID-19 pandemic. The pandemic underscored just how risky it is to rely heavily on physical cash. Suddenly, the mission for DCash felt more urgent than ever. In response, the ECCB launched the DCash pilot in March 2021, across four countries: Antigua and Barbuda, Grenada, Saint Christopher (St Kitts) and Nevis, and Saint Lucia.

The goal was simple yet transformative: to give people in the ECCU a secure, convenient way to send and receive money anytime, anywhere—with just a few taps on their mobile devices. No banks? No problem. Regardless of your location or employment status, DCash was designed to work for you.

How it Worked: Digital Wallets to Meet Different Needs

To make DCash accessible to all, ECCB introduced three types of wallet:

- Registered Wallet: For customers with bank or credit union accounts.

- Value-Based Wallet: For individuals without traditional banking relationships.

- Merchant Wallet: For businesses to send and receive payments seamlessly.

Behind the scenes, ECCB built systems for minting digital currency and managing its distribution, while ensuring continuous security and privacy.

A Team Effort

We did not go it alone.

Eight financial institutions (FIs) in the ECCU partnered with ECCB at the launch—proof of their confidence in DCash’s potential. By January 2024, that number had grown to 21, including 11 credit unions, and over 400 businesses.

At the same time, legislators in all eight countries amended the ECCB Agreement—the legal compact, which, among other things, empowers the ECCB as Monetary Authority for the ECCU. The amendments extended the definition of ‘currency’ to include ‘digital currency’ and conferred the status of legal tender to digital currency issued by the ECCB. These changes were to ensure that users had every assurance about the integrity of DCash.

No journey is without challenges. In January 2022, a system-wide outage tested our resilience and taught us painful lessons about maintaining trust and user confidence amidst innovation. Over the next two years, ECCB worked diligently with its partners to improve and strengthen DCash and, in so doing, enabled us to ‘bounce forward’.

Lessons from the Pilot

The pilot closed in January 2024 and, upon reflection, several key insights emerged:

1. Adoption is not Automatic

Some financial institutions were hesitant about DCash—perhaps seeing it as competition rather than a complement to their services. Others embraced its potential as an affordable way to expand digital offerings for their customers. Similarly, DCash was met by the public with a mixture of excitement, curiosity and skepticism but, mostly, genuine interest about how DCash could make day-to-day life simpler and better. There were teams on the ground in every country working with potential users to help them not only understand DCash, but ultimately to embrace and incorporate it into their daily routines.

2. Prioritise Ease

The value-based wallet (with its simplified onboarding process) attracted twice as many users as the registered wallet, which used more conventional due diligence processes. Automating workflows for user onboarding can be an easy early win in the total user experience.

3. Integration is Key

In the pilot, DCash showed promise as a retail network across the ECCU but highlighted the need for integration with existing payment systems. Without integration, users could face frustration from fragmented services and disjointed experiences involving a mix of automated and manual steps.

4. Be Prepared

The January 2022 outage reminded us that contingency systems are essential for critical payments infrastructure. These systems are vital for both maintaining operational continuity and ensuring that customer-facing services remain uninterrupted during any period of disruption—whether external, such as due to natural disasters, or internal.

5. Digital Finance Success = Ecosystem

Every consumer technology has faced ‘the chicken and egg dilemma’ and DCash was no different. Building digital infrastructure alone is not enough. Success requires an ecosystem where businesses, consumers, payment service providers and financial institutions are individually and collectively better off for having used the DCash system. This means that we must provide compelling value propositions to not only our end users, but also to the various groups of participants, whether governments, businesses, financial institutions or technology developers.

A Bigger Vision: What Role for CBDCs in the ECCU

Across the globe, explorations of CBDCs continue, with central banks—whether large, small or in-between—examining ways in which a CBDC may advance their core mandates. For many central banks, the promise of wholesale CBDCs resonates, while for others there is merit in the retail CBDC model. For the ECCB, CBDCs can play a dual role in helping to modernise the payments infrastructure at both macro and retail-financial system levels.

Beyond increased convenience and speed for everyday users, CBDCs offer something critical: protection of monetary sovereignty in an era where private cryptocurrencies are gaining ground. Cryptocurrencies have shown some potential to ‘rewire’ the global financial system. More concerning, they show the potential to create a shadow financial system without the necessary safeguards and oversight that can protect and stabilise our interconnected financial systems. What this means is that, in the absence of these protections—but with high volatility present and limited if any actionable means of redress—catastrophic consequences for both major institutions and ordinary users can ensue.[1]

Using CBDCs for cross-border transactions is among the ways that this innovation can help the ECCU to stay connected with the wider globe. Integration with other CBDC systems and other payment infrastructures is a prerequisite to see this become a reality. With cross-border transactions, CBDCs can bring their competitive advantages, including speed, payment efficiency, low transaction costs and settlement finality—a likely boon for our region in accessing the goods and services that we do not produce and receiving the remittances that are integral to our economies.

A Call to Action

As we plan for the next iteration of DCash—DCash 2.0—a secure, scalable and commercially deployed solution, we invite you to be a part of the journey. We believe that we must build the change we want to see. As members of the ECCU, we all are its architects. Stay connected by signing up for updates on the development of DCash 2.0. Participate in our periodic surveys and focus groups and share your expectations. If you own a business, or are looking to start one, tell us how you would like DCash to support your venture through visionary tools and other expertise. Whether you are a payment service provider, a fintech developer, an NGO or non-profit organisation, your voice is welcomed.

As we look ahead, one thing is clear: DCash is just the beginning of a more inclusive digital economy in the Eastern Caribbean. Our future progress depends on working together—we invite you to join us in shaping this exciting future. The costs of stagnation or regression are much too high.

WE WOULD LIKE TO HEAR FROM YOU!

We value your thoughts! To help us make this blog series even better, we’ve put together a very short survey—just five quick questions. Your feedback will help us create more content that’s relevant, engaging, and useful to you. It will take no more than two minutes. Click here to access the survey. Thank you for being part of our community!

---

About the Eastern Caribbean Central Bank

The Eastern Caribbean Central Bank (ECCB) was established in October 1983. The ECCB is the Monetary Authority for Anguilla, Antigua and Barbuda, the Commonwealth of Dominica, Grenada, Montserrat, Saint Christopher (St Kitts) and Nevis, Saint Lucia and Saint Vincent and the Grenadines.

Disclaimer

The ECCB strongly supports academic freedom and encourages such activity among its employees. Notwithstanding, the views and opinions expressed are solely those of the authors. The ECCB may not necessarily endorse the writers’ position or guarantee technical accuracy. Readers are free to submit their comments or questions on the information presented in this publication.

References

Baker, J. (2024, October 3). Wholesale versus retail CBDCs in cross-border payments. FXC Intelligence. Retrieved from https://www.fxcintel.com/research/analysis/ct-wholesale-versus-retail-cbdcs

International Monetary Fund. (2018). Future of Work: Measurement and Policy Challenges. Retrieved from https://www.imf.org/external/np/g20/pdf/2018/071818a.pdf.

[1] Notwithstanding, cryptocurrencies have provided some insights into the ways that CBDCs can evolve to better serve users in a deeply interconnected digital world. Many central banks also recognise that a digital finance future is likely to include both CBDCs and the cryptocurrency ecosystem, with the potential for CBDCs to offer a bridge between the worlds of traditional finance and digital finance.

[1]The gig economy refers to services—whether physically or digitally delivered—by independent workers in an on-demand or short-term basis. Globally, their popularity has grown for a number of reasons including increased marketplace platforms such as Uber, DoorDash and InstaCart (IMF, 2018).